-

Enrollment Periods

Enrollment Periods

Understanding Medicare Enrollment Periods

At-A-Glance

There are certain times when you can sign up for Medicare. You should enroll on time. If you wait to sign up, you may have to pay penalties when you do join.

When Can I Enroll in Medicare?

There are several times when you can enroll in Medicare, and each of those times has certain rules around applying and when your coverage will begin. Understanding when you can enroll and the best time to do so is an integral part of getting your Medicare.

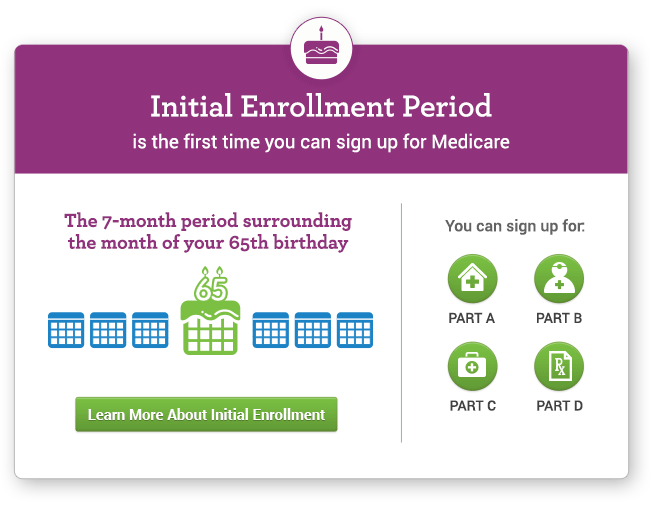

Initial Enrollment Period

There are several times when you can enroll in Medicare, and each of those times has certain rules around applying and when your coverage will begin. Understanding when you can enroll and the best time to do so is an integral part of getting your Medicare.

- The 3 months before your 65th birthday,

- The month of your birthday, and

- The 3 months after your birthday.

Your coverage will start no sooner than your birthday month.

Example: If your birthday is in July, your Initial Enrollment Period begins April 1 and ends October 31.

If you miss this period, you will have a chance again later on. But if you wait, you may have to pay more. You also could be without health coverage.

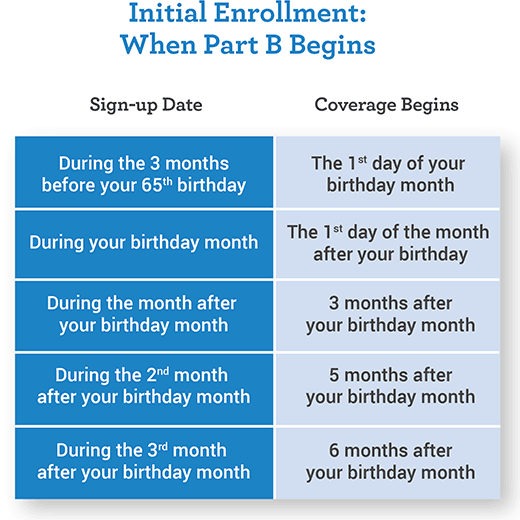

When does my Part B coverage begin?

The start date of your coverage will depend on which month you enrolled in Part B during the Initial Enrollment Period.

Example: John turns 65 on May 6. Therefore, his IEP is from February to August. If John signs up for Part B:

- During February, March or April, his coverage starts May 1 (his birthday month)

- During May, his coverage starts June 1

- During June, his coverage starts August 1

- During July, his coverage starts October 1

- During August, his coverage would not start until November 1

If your birthday falls on the 1st day of any month, and you enroll during the 3 months before your birthday, your coverage will begin on the 1st of the month prior to your birthday.

Example: Gail’s birthday is December 1. She applies for Medicare in September, and her coverage starts November 1.

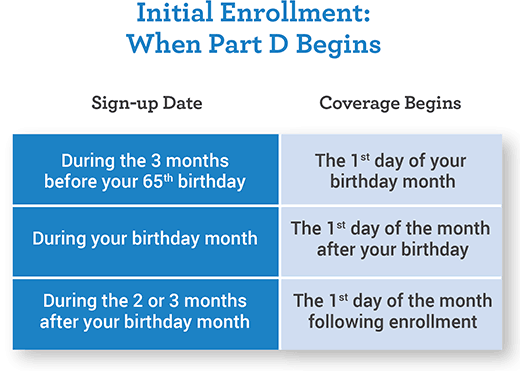

When does my Part D (prescription drug plan) coverage begin?

The start date of your Part D coverage again depends on when you enroll.

Example: Keeping with the example above, John turns 65 in May. His Part D IEP is the same 7-month period surrounding his 65th birthday as his Part B IEP. His IEP is from February to August. John’s Part D coverage cannot start before his Part A and/or B begins. If John enrolls in Part D:

- During February, March or April, his coverage starts May 1

- During May, his coverage starts June 1

- During June, his coverage starts July 1 (but not before his Part A and/or B)

- During July, his coverage starts August 1 (but not before his Part A and/or B)

- During August, his coverage starts September 1 (but not before his Part A and/or B)

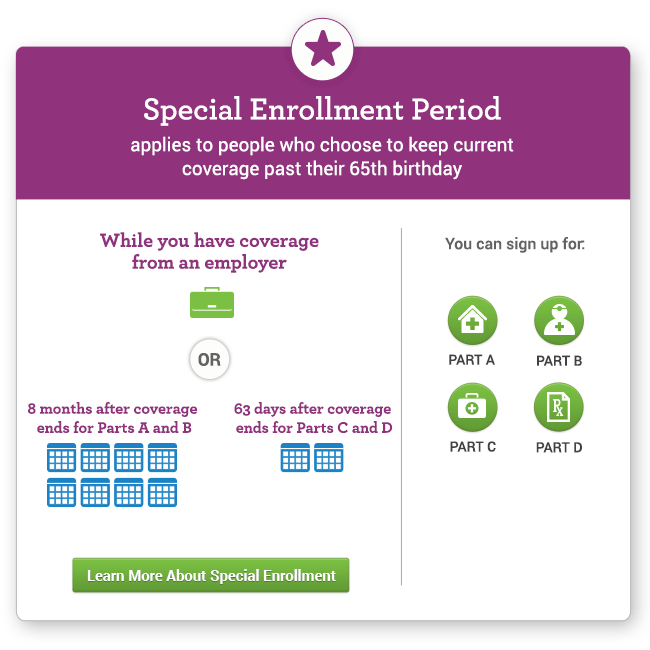

Special Enrollment Period

There are Special Enrollment Periods (SEPs) that apply when you are able to delay your enrollment in Medicare Parts A, B, C & D. These SEPs are only available for certain circumstances.

Special Enrollment for Parts A and B

You may have waited to sign up for Medicare Part A (hospital service) and/or Part B (outpatient medical services) if you were working for an employer with more than 20 employees when you turned 65, and had healthcare coverage through your job or union, or through your spouse’s job.

You can get a Special Enrollment Period to sign up for Parts A and/or B:

- Any time you are still covered by the employer or union group health plan through you or your spouse’s current or active employment, OR

- During the 8 months following the month the employer or union group health plan coverage ends, or when the employment ends (whichever is first).

If you wait longer, you may have to pay a penalty when you join.

If you are disabled and working (or you have coverage from a working family member), the Special Enrollment Period rules also apply as long as the employer has more than 100 employees.

Special Enrollment for Parts C and D

You may have waited to sign up for Medicare Part C or Part D if you were working for an employer with more than 20 employees when you turned 65, and had healthcare coverage through your job or union, or through your spouse’s job. The Special Enrollment Period for Part C (Medicare Advantage Plan) and Part D (drug coverage) is 63 days after the loss of employer healthcare coverage.

You can get a Special Enrollment Period to sign up for Part C (must enroll in Parts A & B too):

- During the 63 days after the employer or union group health plan coverage ends, or when the employment ends (whichever is first).

You can get a Special Enrollment Period to sign up for Part D (must enroll in Part A and/or B too):

- During the 63 days after you or your spouse’s employer/union or Veteran’s Administration coverage ends, or when the employment ends (whichever is first).

Certain events trigger other Special Enrollment Periods for Part D plans. For example, you can switch plans if:

- You move out of the area your current plan serves, OR

- You enter, leave or live in a nursing home, OR

- Your plan changes and no longer serves your area, OR

- You get Extra Help with your Medicare prescription drug costs.

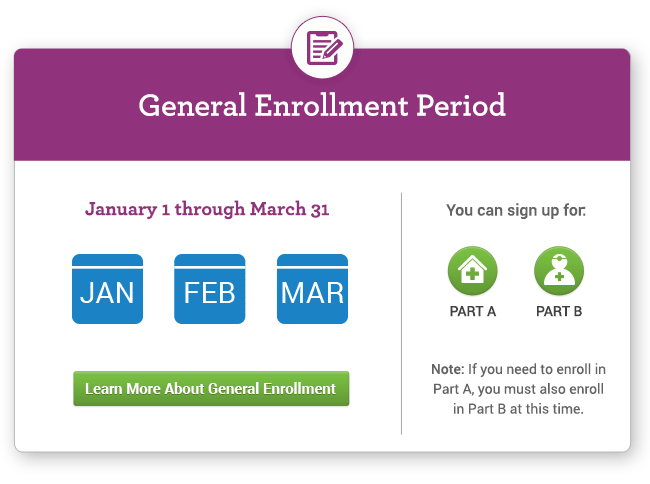

General Enrollment Period

If you miss your Initial Enrollment Period or your Special Enrollment Period, you get another chance to enroll.

You can sign up for Medicare Parts A & B between January 1 and March 31 each year. Your Medicare coverage would begin on July 1 of the same year. It is important to note that if you need to buy Part A, you must also enroll in Part B at this time.

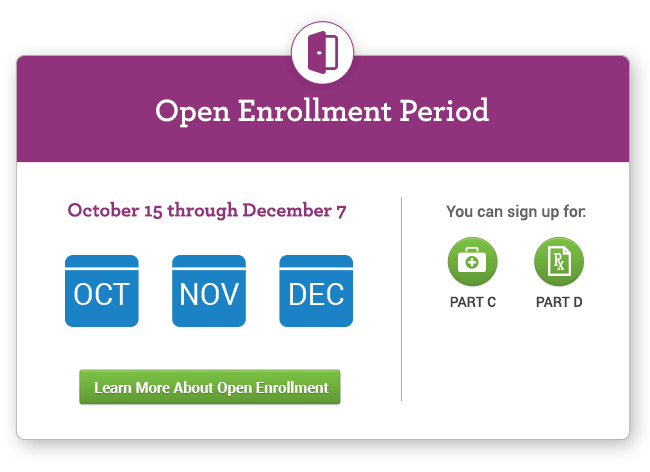

Open Enrollment Period

The Open Enrollment Period – sometimes called the Annual Election Period or Annual Coordinated Enrollment Period – runs each year from October 15 to December 7. During this time, Anyone with Medicare Parts A & B can switch to a Part C plan, anyone with Medicare Part C can switch back to Parts A & B, anyone who has or is signing up for Medicare Parts A or B can join, drop or switch a Part D prescription drug plan, anyone with Medicare Part C can switch to a new Part C plan. Your coverage will start January 1 of the following year.

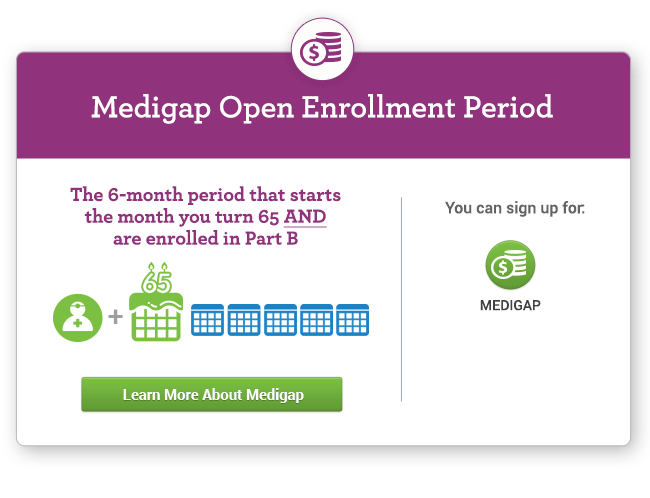

Medigap Enrollment Period

It’s recommended that you buy a Medigap policy during your 6-month Medigap open enrollment period, because during this time, you can buy any Medigap policy sold in your state, even if you have health problems. This period automatically starts the month you’re 65 or older and enrolled in Medicare Part B.

If you apply for Medigap coverage after your open enrollment period, there’s no guarantee that an insurance company will sell you a Medigap policy if you don’t meet the medical underwriting requirements, unless you’re eligible due to a special situation.

If you have Parts A & B (Original Medicare) and a Medigap policy, you should weigh your decisions very carefully before switching to a Medicare Advantage plan. You may have difficulty getting a Medigap plan again in the future if you decide to switch back.

Be aware that if you did not sign up for Medicare when you were first eligible and did not have other insurance, you may face a penalty for late enrollment.