-

Medicare Supplements (Medigap)

Medicare Supplements (Medigap)

What is Medicare Supplement Insurance (Medigap)?

Medicare Supplement or "Medigap" is designed to pay for all of the areas that Original Medicare does not cover. Based on product line selected, Medigap could potentially pay all copays and deductibles, leaving you with virtually no out-of-pocket expense, as well as provide additional benefits over and beyond what Traditional Medicare was ever meant to cover.

Many companies sell Medigap plans but each company must sell the exact same benefits, or standard benefits, of each plan. For example, a Medigap Plan C sold by Company X must have the same benefits as Plan C sold by Company Y. Although the company can request additional benefits over and above other companies to try and differentiate themselves from others, these benefits must be approved by the State in order for the company to recognize these as additions. Another area companies try to differ themselves is in the cost, or premium. Beware, some companies try to underbid their competition in price but do so in a very interesting manner that is necessary to understand prior to selecting a plan to avoid any buyer's remorse.

Be sure to contact us so we can assure you you’re not paying more than you need for your Medigap coverage and are choosing the product lines, type, and carrier you desire.

Which is the Best Plan?

There isn't one “best” Medigap plan. A specific Medigap plan might work for you if it offers coverage that works for your needs and comes with premiums that fit your budget.

Medigap Plan F is the most popular Medicare Supplement Insurance plan. 49 percent of all Medigap beneficiaries are enrolled in Plan F.

Plan F covers more standardized out-of-pocket Medicare costs than any other Medigap plan. In fact, Plan F covers all 9 of the standardized Medigap benefits a plan may offer.

The average Plan F premium in 2018 was $169.14 per month.

Medigap Plan G is the second most popular Medigap plan, and it is quickly growing in popularity. Plan G enrollment spiked 39 percent in recent years.

Medigap Plan G covers all of the same out-of-pocket Medicare costs than Plan F covers, except for the Medicare Part B deductible. The 2021 Part B deductible is $203 per year ($16.92 per month).

This means that if you find a Medigap Plan G option that costs only $16.92 more per month (or less) than Plan F, it might be a better value over the course of the year than Plan F if you meet the Part B deductible.

The average Medigap Plan G premium in 2018 was $122.78 per month.

Your unique health coverage needs and budget are important factors to consider as you shop for Medicare Supplement Insurance plans.

The potential cost predictability a Medigap plan can bring may be able to help you better predict your monthly health care spending.

You can combine a Medigap plan with a Medicare Part D prescription drug plan, which can help cover your costs for retail prescription drugs.

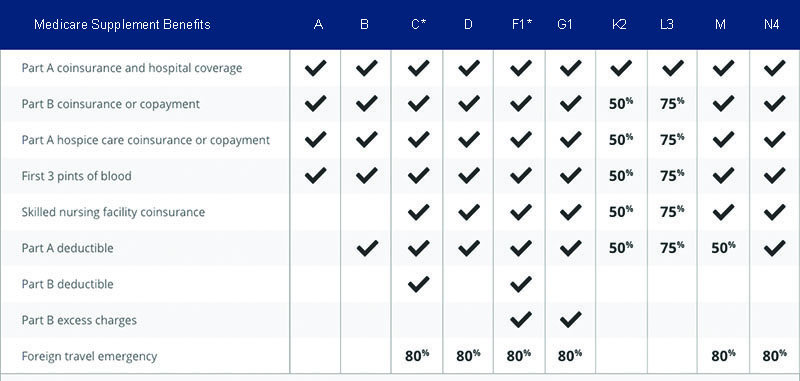

Learning how to compare Medicare Supplement plans is fairly easy. Medicare publishes a booklet each year that includes this Medicare Supplement Plans comparison chart. The Medigap comparison chart allows you to see and compare Medicare Supplement plans side by side. The Medicare Supplement comparison chart below shows you exactly which benefits each plan covers.

Plan F and Plan C are not available to Medicare beneficiaries who became eligible for Medicare on or after January 1, 2020. If you became eligible for Medicare before 2020, you may still be able to enroll in Plan F or Plan C as long as they are available in your area.

Plans F and G offer high-deductible plans that each have an annual deductible of $2,490 in 2022. Once the annual deductible is met, the plan pays 100% of covered services for the rest of the year. The high-deductible Plan F is not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020.

Plan K has an out-of-pocket yearly limit of $6,620 in 2022. After you pay the out-of-pocket yearly limit and yearly Part B deductible, it pays 100% of covered services for the rest of the calendar year.

Plan L has an out-of-pocket yearly limit of $3,310 in 2022. After you pay the out-of-pocket yearly limit and yearly Part B deductible, it pays 100% of covered services for the rest of the calendar year.

Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to $50 copayment for emergency room visits that don’t result in an inpatient admission.

Medicare Supplement Plans Comparison Chart: 10 Plan Options

The Medigap Plans comparison chart above compares all of the plans side by side. This allows you to see which ones have the most benefits, and which ones cover the least. As mentioned above, Plan F and Plan G cover the highest percentage of benefits, leaving you with very little out-of-pocket. Below is a list with a brief overview on each plan so that you can compare Medicare Supplement plans easily:

Medigap Plan A

Medigap Plan A offers the most basic of all the Medigap plans. Even still, it will cover the 20% that Medicare doesn’t pay for on outpatient treatments. That’s arguably the most important piece of all Medigap plans. All Medicare insurance carriers must offer Plan A. However, some states do not require companies to offer it to people under age 65 on Medicare disability.

Medigap Plan B

Medigap Plan B covers everything that Plan A covers but it also picks up the Medicare Part A hospital deductible. Plan B is a Medigap plan that pays after Medicare pays. Don’t confuse it with Part B, which is part of your Original Medicare benefits that pays for outpatient medical.

Medigap Plan C

Medigap Plan C is one of the most comprehensive supplements. It covers everything except Medicare excess charges. This means it pays both of your deductibles and the 20% that you would normally owe toward all outpatient expenses. Medigap plans C & F are very popular.

Medigap Plan D

Plan D covers most things but does not pay the Part B deductible nor any Medicare excess charges. This makes it one of the least popular Medigap plans. Don’t confuse it with Part D, which is your drug coverage – two different things.

Medigap Plan F

Medigap Plan F has long been the most popular selling Medigap plan in the Medicare Supplement world. It covers ALL of the items that you would normally pay. It leaves you with nothing out-of-pocket for covered services. Many people enjoy the peace of mind that comes with knowing you won’t even owe a copay for doctor visits or hospital stays.

There is also a high-deductible version of Plan F that provides great Medigap coverage after you meet a deductible first.

Medigap Plan G

Medigap Plan G has been gaining in popularity in recent years. It covers everything that Plan F does except for the Part B deductible. Premiums for Plan G are often very competitive, which can often make it a better value than Plan F. When we compare Medicare Supplements between Plan F and G in most states, we often find that Plan G is a better value annually.

Medigap Plan K, L, M

These plans offer partial coverage of certain benefits. For instance, Plan K covers 50% of most items and Plan L covers 75% of most items. All three of these plans are rarely requested by Medicare beneficiaries, so not all carriers offer them. However, you can often find good Medicare Supplement rates for these plans in certain areas.

Medigap Plan N

Medigap Plan N was created in 2010. It offers lower premiums in exchange for you paying copays for certain things like doctor and emergency room visits. It also does not cover the Medicare excess charges. The lower premiums have been attractive to many beneficiaries, but we sometimes find that policyholders find the small bills for excess charges to be annoying.

When you are learning how to compare Medicare Supplement plans, just remember that Plan N is the one that requires copays from you for doctor and E.R. visits. That’s why the premiums are lower. People interested in the Medigap policies which offer the most affordable rates are usually interested in Plan N.